Specific tax. Types of taxes

Taxes- These are funds collected by the state from citizens (so-called individuals) and organizations (so-called legal entities). Taxes are the basis for filling the revenue side of the country's budgets.

Establishment level

Depending on the size of the part of the state in which the collection of a separate tax is established, and on the type of budget to which taxpayers transfer the collected funds, all taxes are divided into several types:

Method of withdrawal

Direct– taxes that are collected from the income of an individual or legal entity. Direct taxes may include the following: income tax (NPO) of organizations, tax on personal income. The direct tax is paid by the “agent” of the economy who received the income.

The most obvious example is corporate income tax. When a company engages in business, it has income (the amount of revenue from sales of goods, works and services to its customers) and expenses (the costs that the organization incurs to generate income). The difference between these amounts is the organization's profit. The more profitable the organization, the greater the amount of tax paid.

Indirect taxes are “inside” the price of goods and services. When selling, the selling organization calculates the required amount of tax and transfers it. Thus, the seller pays the tax, but at the expense of the buyer who will use this product or service (since the buyer paid for the product or service, including applicable taxes). This is the key difference between indirect tax and direct tax. As an example, when purchasing a bottle of wine in a grocery store, the buyer pays:

- the cost of the product itself;

- excise tax on alcoholic products;

The amount of VAT paid by the buyer on a retail purchase can often be seen on the sales receipt.

Subject of taxation

Depending on who the state collects the tax from, we can distinguish the following groups:

- Taxes on legal entities the state receives from organizations registered in the Russian Federation, including Russian companies and representatives of foreign capital represented in the Russian economy (having representative offices and branches). The above-mentioned income tax, the rather rare gambling tax and many other taxes are included in this group.

- Personal taxes levied on individual taxpayer citizens. The tax of this group can be levied both on citizens of the Russian Federation and on citizens of other states who received income in the territory of the Russian Federation. Income and property taxes are collected from individuals.

- Mixed taxes can be collected from all categories of taxpayers. For example, VAT must be paid by all consumers of goods and services.

It is worth noting a special category of individuals - individual entrepreneurs or individual entrepreneurs. A person, being an individual, pays all taxes provided for individuals. But if he is engaged in commercial activities and is registered in the prescribed manner, he also pays other taxes.

Depending on the taxation system chosen by the entrepreneur (general, simplified or special types), this may be VAT, income tax, tax levied under simplified or patent systems, and so on.

According to their purpose, taxes are divided into are common And targeted(special). General taxes are collected in budgets “in a common pot” and are used at the discretion of the body that manages the budget. Targeted taxes are used for a specific purpose. For example, transport and land taxes can be collected into appropriate local funds and spent specifically on road repairs or territory development.

Source of payment

Based on the source of payment, taxes are divided into:

- Included in cost(goods, works or services) – taxes that relate to the costs of producing products or services. Examples could be the transport tax of a bus fleet, payments to an oil company for the use of subsoil, as well as contributions related to the wages of the organization's employees. The amount of taxes of this type paid does not depend in any way on the amount of income, but often depends on the amount of individual types of expenses.

- Included in revenue– taxes such as the income tax of commercial organizations and the “simplified” tax in the “income-expenses” option. There is a dependence on both the income received and the actual expenses of the organization.

- Tax based on income- a tax that is determined only by the taxpayer’s income and is not affected in any way by the amount of expenses. As an example, the tax on the income of an individual entrepreneur on a “simplified” basis with the object of taxation “income”.

Object of taxation

Calculus methods

Taxes may be progressive(if the tax rate increases as a percentage when the object of taxation in rubles increases) and regressive(tax rate falls). A regressive tax is stimulating.

Taxes may be progressive(if the tax rate increases as a percentage when the object of taxation in rubles increases) and regressive(tax rate falls). A regressive tax is stimulating.

Today, there are no examples of taxes of the first type in the tax system of the Russian Federation, although the possibility of introducing a progressive method and a complex scale for personal income tax is regularly discussed.

Almost all taxes in the Russian Federation are proportional(this means that the rate remains unchanged when the size of the taxable object changes), for example:

- for most goods and services, the VAT rate is 18% of the amount of goods sold or services provided;

- the state will take 20% of the organization’s profits;

- Almost any income of individuals is taxed at a rate of 13%.

Also, according to the calculation method, fixed and graduated taxes are distinguished:

- Magnitude flat taxes does not depend at all on the value of the taxable object or actual income. For example, the rate of a tax such as a transport tax is determined by the power (in horsepower or kilowatts) of the vehicle and does not depend in any way on its cost. Hard taxes also include water tax and many types of excise taxes.

- Stepped taxes: The rate changes depending on the amount of income. An example of a graduated tax could be a contribution to the Social Insurance Fund (FSS), paid by an organization and calculated from the income of an employee of the organization (although this is not exactly a tax). The contribution rate is 2.9% if the employee’s total income does not exceed a certain base (today – 718 thousand rubles); if the base is exceeded, no tax is levied. Thus, the contribution to the Social Insurance Fund is regressive (as income increases above the specified base, the total percentage of the contribution charged decreases). By introducing a maximum tax base, the state stimulates the “whitening” of wages - it becomes more profitable for the organization to pay higher wages.

Who counts the amount charged?

According to the method of taxation, the subjects of this article are divided into cadastral(they are also non-cash) and declaration(cash). Cadastral taxes are calculated by the tax authorities themselves based on available information about the value of the taxable object. For example, for individuals, all taxes related to property are cadastral. Including:

- Transport tax(tax inspectors receive information about whether individuals own vehicles from the State Traffic Safety Inspectorate).

- Property tax, and land tax(the tax service receives the cadastral value of real estate from the database of the Federal Service for State Registration, Cadastre and Geography - Rosreestr).

The Tax Service annually calculates the amount of tax and sends out notifications to taxpayers about the need to pay cadastral taxes. In contrast, return taxes are calculated based on data provided by the taxpayer himself. For example, if a citizen resells a recently purchased apartment, then he is obliged to independently draw up an income statement, send it to the tax authorities and pay the appropriate amount of tax.

In order of inclusion in the budget

Legislation may prescribe the procedure for paying the same tax to budgets of different levels (federal, local, regional - it happens that taxes are paid to all three). If this order continues for a long time, then the tax is fixed.

Legislation may prescribe the procedure for paying the same tax to budgets of different levels (federal, local, regional - it happens that taxes are paid to all three). If this order continues for a long time, then the tax is fixed.

If the procedure is regularly reviewed, then this regulating tax. An example of the latter is the tax on the actual profit of companies, the procedure for posting it has changed several times.

Today, the basic rate is 20%, of which 18% is transferred to local budgets and only 2% to the federal budget. An example of a fixed tax is a transport tax, which is always transferred to local budgets.

Order of reference

According to the order of administration, taxes are divided into generally binding(collected throughout the country - excise taxes, NGOs, etc.) and optional(introduced by individual regions, UTII as an example).

In addition, each region has the right to optionally introduce benefits for certain taxes (for example, taxes for “simplified people”). It is impossible not to mention Skolkovo - on the territory of this technology park there are many benefits for residents.

Fines and penalties for violating tax laws

An important condition for the viability of the state economy is the mandatory and timely payment of accrued taxes by all taxpayers. If payment is late, and even more so if payment is evaded, the tax service may impose fines and penalties on unscrupulous taxpayers.

For example, the penalty for late payment of VAT by an organization is 1/300 of the Central Bank rate for each calendar day of delay(this is about 12% per annum). If a taxpayer evades paying tax, the tax office may impose a fine of 20 to 40% of the amount of unpaid tax.

For legal entities and entrepreneurs. What are they? And what is better to choose in this or that case? Every individual entrepreneur should know the pros and cons of existing tax payment systems. Otherwise, the business may fail. All this and more will definitely be discussed further. In the end, everyone will understand how to choose one or another taxation system. It's not as difficult as it might seem at first glance.

Taxation is...

First, let's figure out what we basically have to deal with. Taxation for individual entrepreneurs and LLCs is an extremely important component. This is a tax payment system. Thanks to it, income is declared and part of the profit is transferred to the state.

According to the Tax Code of the Russian Federation (Article 17), tax payment systems are determined by:

- objects of taxation;

- tax base;

- the period for which you need to pay;

- tax rate;

- payment calculation procedure;

- terms and methods of money transfer;

- benefits and other tax features.

At the moment, a legal entity may face different types of taxation. Next, we will look at each possible option with its pros and cons.

Types of systems

Let's start with a short list. It will help you understand from which you can generally choose the type of transfer of part of the profit for doing business.

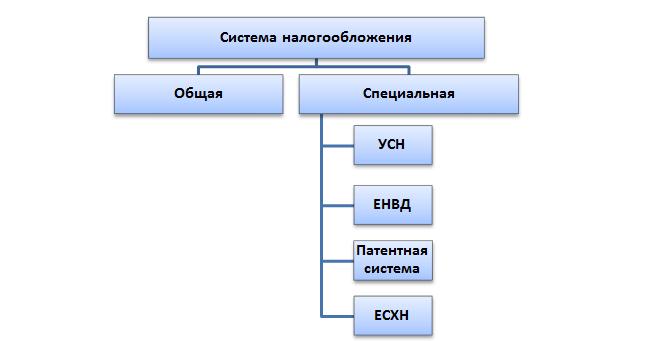

Currently in Russia there are the following types of taxation:

- OSNO;

- USN (simplified);

- UTII (imputation);

- Unified Agricultural Sciences;

Unified agricultural tax is almost never used in practice. Therefore, you should not focus much attention on it. Let's look at other types of taxation and their characteristics. It is not difficult to understand all this.

OSNO and business

The most common scenario is the use of a common taxation system. It is selected by LLC or Individual Entrepreneur by default. The arrangement is not always profitable, especially at the very beginning of a business.

It involves serious paperwork and very large taxes. Therefore, many entrepreneurs often refuse OSNO. For some, this option is suitable.

To briefly describe the tax payment system, in this case you will have to transfer funds for the organization’s property and income. VAT also applies. It is this component that allows you to choose or refuse OSNO.

Disadvantages of the general system

We have listed the main types of taxation in Russia. Now it’s worth considering each option in more detail.

At the moment, OSNO has the following weaknesses:

- high taxes;

- variety of payments;

- serious tax reporting.

That's all. There are no more shortcomings.

It is worth paying attention to the fact that an LLC (company) under OSNO pays a profit tax of 20%, and an individual entrepreneur - 13%. Quarterly reporting. And therefore it causes a lot of trouble for companies.

Pros of OSNO

Now about the positive aspects. They play an important role. Especially if a person does not know what type of tax payment to choose.

The general tax system in Russia today has the following advantages:

- applies everywhere and to any type of activity;

- You don’t have to contact the Federal Tax Service additionally to select it;

- allows you to reduce VAT on VAT that is transferred to suppliers;

- the tax base is profit minus expenses;

- in some cases, personal income tax can be from 0 to 30%.

However, this option is not always used. What type of taxation should I choose in this or that case? To do this, you should pay attention to other offers. Only then will the entrepreneur be able to figure out how best to transfer taxes to the state treasury.

simplified tax system in Russia

The next tax payment system is the simplified tax system. It is called "simplified". This is the layout most often used by entrepreneurs.

Already from the name of the system it is clear that this tax payment regime implies a simplified procedure. That’s right - the paperwork with it is minimal, especially if the citizen works without employees.

The simplified tax system has 2 varieties. More precisely:

- income - expenses;

- income.

Depending on the type chosen, the tax base will change. In the first case, net profit is meant (after deducting expenses), in the second - all income received.

"Simplified" provides for the payment of personal income tax. They pay either from 5 to 15% (income - expenses), or from 0 to 6% (income). The exact amount of tax depends on the region in which the entrepreneur lives, as well as on the type of activity.

Disadvantages of the simplified tax system

A few words about why individuals refuse the “simplified approach”. This arrangement is not suitable for everyone.

For example, due to similar shortcomings:

- not all types of activities allow the use of the simplified tax system;

- you have to write additionally ;

- the company can employ no more than 100 people;

- you need to receive no more than 60 million rubles per year (since 2017 - 120,000,000) to be eligible for the simplified tax system.

Accordingly, this type of taxation is quite often suitable for individual entrepreneurs working for themselves without employees. But what are the advantages of this system?

Advantages of the simplified tax system

"Simplified" is a favorite direction in which entrepreneurs work. Small companies also often settle on this arrangement, but over time they have to abandon it due to the large number of employees and high profits.

The advantages of the simplified tax system include:

- minimal paperwork;

- low tax rates;

- the possibility of reducing taxes by the amount of contributions to the Pension Fund;

- the right to choose the method of calculating the tax base.

In practice, if it is possible to use the “simplified” version, citizens try to settle on this option.

Reporting is annual (until May 31 for companies and until April 30 for individual entrepreneurs), but you will have to pay personal income tax once a quarter. Additionally, you will have to keep a ledger of expenses and income.

The tax base is reduced through the costs of maintaining the company, contributions for employees to the Pension Fund (no more than 50% of transfers) and for yourself (100% of the amounts paid to the Pension Fund).

UTII, or "imputation"

And there is such a thing as UTII. This is popularly called “imputation”.

UTII is a type of taxation that is not used in Moscow. But in other regions of the Russian Federation you can actively work with it. It provides for the absence of any taxes depending on the income of the enterprise.

The types of taxation for LLCs, of all those previously listed, are not as interesting to businessmen as UTII. "Vmenenka" is ideal for cafes, taxis and a number of other types of activities.

As in the case of the simplified tax system, UTII can be reduced by the amount of fixed deductions. Reporting and payment of taxes in this mode is quarterly. Taxes are paid depending on the potential profit of an individual entrepreneur or LLC. The corresponding estimated income is established by the state and depends on the region of registration, as well as on the activities of the enterprise.

About the shortcomings of UTII

What are the disadvantages of “imputation”? After all, all types of taxation have strengths and weaknesses. Every businessman needs to remember them.

At the moment, UTII has the following disadvantages:

- not applicable in all regions;

- can only be used for certain types of activities;

- in some cases, working with UTII is not entirely profitable;

- paperwork from quarter to quarter with the payment of taxes;

- You cannot work with UTII if the company has more than 100 subordinates.

In addition, as in the case of the simplified tax system, when “imputed” another company’s share in the business should not exceed 25%. Otherwise, the right to the considered type of tax payment is abolished.

About the advantages of UTII

Types of taxation for LLCs and for entrepreneurs necessarily include “imputation”. This is not the worst option. Especially if the company's real profit is greater than the government assumes.

The following strengths of “imputation” can be noted:

- the tax base does not depend on the company’s income;

- no additional expenses are required except for fixed contributions to the Pension Fund;

- it is possible to reduce taxes on contributions made to extra-budgetary funds;

- You don't have to use cash registers.

Important: the tax amount is determined by 15% of the company’s potential annual profit.

PSN is...

Not long ago, patent taxation appeared in Russia. The types of activities in this case are also limited, as with the simplified tax system or UTII. Nevertheless, PSN is actively used in practice. Especially if a person wants to open an individual entrepreneur and “see” how he can conduct his business.

In general, the PSN resembles the simplified tax system or “imputation”, but with its pros and cons. For example, this option is available only to individual entrepreneurs. And the amount of tax does not depend on the actual profit of the entrepreneur.

Disadvantages of Patents

Now let's look at the disadvantages of this option. As already mentioned, PSN is available only to entrepreneurs. LLCs will not be able to work with her under any circumstances.

At the moment, the patent system has the following weaknesses:

- can be used for some types of activities;

- not always profitable;

- the company should not have more than 15 employees;

- it is impossible to reduce taxes on mandatory contributions to the Pension Fund;

- annual profit cannot exceed more than 60,000,000 rubles;

- The cost of a patent is different in all regions of the Russian Federation.

Nevertheless, this arrangement seems very attractive to some. In order to decide on the choice of tax payment system, you need to evaluate all the pros and cons of each proposal. This is the only way a person will make the right decision.

Pros of a patent

Types of taxation for LLCs do not provide for PSN. But entrepreneurs may face this situation.

Patents are convenient. But why? It is customary to highlight the following positive aspects of the regime:

- there is no dependence of the tax amount on real profit;

- minimal paperwork;

- there is no need to use cash registers;

- you can buy a patent for a period of 1 to 12 months;

- taxes are paid either before the expiration of the patent (if it was purchased for a period of up to six months), or 33% of the amount is transferred no more than 90 days after acquisition, and the balance - until the end of the validity of the individual entrepreneur's PSN;

- It is allowed to register several patents at once.

Accordingly, today many entrepreneurs pay attention to PSN. In particular, if this regime is applicable to a particular type of activity.

Unified agricultural tax

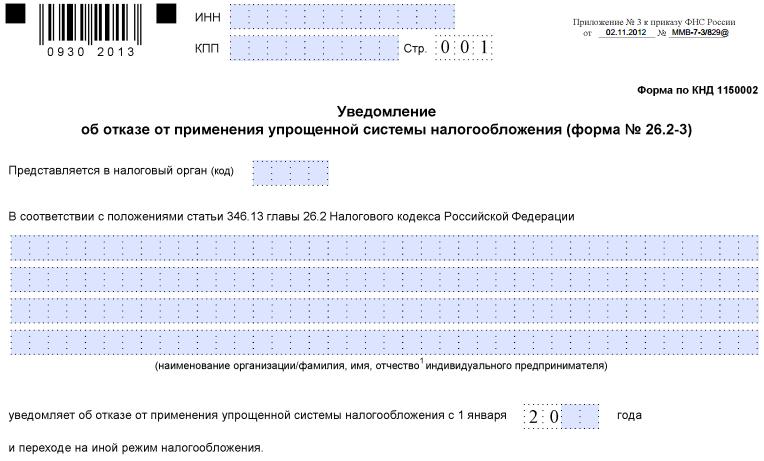

When switching to a new tax payment regime, a citizen is required to write an application within the established time frame (usually from 10 to 30 days from the beginning of the tax period) and submit it to the Federal Tax Service. You will have to indicate the tax type code and the type of company activity. All this can be viewed in the tax service databases.

What is Unified Agricultural Tax? A tax that is only suitable for those who independently conduct agricultural activities. Almost never occurs in real life. Accordingly, we will not consider such a regime. It is enough to know that it exists. It is better to check with the Federal Tax Service for more detailed information.

Conclusion

We found out what types of taxation for individual entrepreneurs and companies exist in Russia. But what is better to stop at?

Based on all of the above, we can conclude that the simplified tax system, UTII and PSN are similar to each other. Therefore, they need to be compared for a specific type of activity in a particular region.

We can only say with confidence that it is better not to agree to OSNO at first. For inexperienced businessmen, this is a huge tax and reporting burden that can ruin their business.

Tax- a mandatory, individually gratuitous payment forcibly collected by government bodies of various levels from organizations and individuals for the purpose of financial support for the activities of the state and (or) municipalities.

Taxes should be distinguished from fees (duties), the collection of which is not gratuitous, but is a condition for the performance of certain actions in relation to their payers.

The collection of taxes is regulated by tax laws.

The totality of established taxes, as well as the principles, forms and methods of their establishment, modification, abolition, collection and control form the tax system of the state.

In the Russian Federation there are three types of taxes: federal, regional and local.

The list of taxes of each type is established by the Tax Code of the Russian Federation.

Government bodies do not have the right to introduce additional taxes or mandatory deductions not provided for by the legislation of the Russian Federation, as well as to increase the rates of established taxes and tax payments.

Elements of tax

Before levying a particular tax, the state, represented by legislative or representative authorities, must define the elements of the tax in legislative acts.

Elements of tax are the principles of construction and organization of taxes.

The elements of the tax include:

taxpayer;

the tax base;

unit of taxation;

calculation order;

tax salary;

source of tax;

taxable period;

payment procedure;

tax payment deadline.

Types of taxes

All taxes are divided into several types:

Direct and indirect taxes

Taxes are divided into direct, that is, those taxes that are levied on economic agents for income from factors of production, and indirect, that is, taxes on goods and services, consisting of the very price of consumer goods.

Direct taxes include personal income tax and similar taxes.

Indirect taxes include value added tax, excise taxes and other taxes.

Credit and income taxes

It is also customary to distinguish between lump sum and income taxes.

The state sets cord taxes regardless of the income level of an economic agent.

Income taxes mean taxes that make up a certain percentage of income.

This relationship is shown either by the marginal tax rate, which explains how much the tax increases when income increases by one monetary unit, or by the average tax rate: simply the ratio of the amount of tax levied to the amount of income.

Progressive, regressive or proportional taxes

Income taxes themselves are divided into three types:

Progressive taxes are taxes in which the average tax rate increases as income level increases. Thus, if the agent's income increases, then the tax rate also increases. If, on the contrary, the amount of income falls, then the rate also falls;

Regressive taxes are taxes whose average tax rate decreases as income levels increase. This means that when the income of an economic agent increases, the rate falls, and, conversely, increases if income decreases;

Proportional taxes are taxes whose rate does not depend on the amount of taxable income.

Basic functions of taxes

Taxes simultaneously perform four main functions: fiscal, distribution, regulatory and control.

The fiscal function of taxation is the main function of taxation. Historically, the most ancient and at the same time basic: taxes are the predominant component of state budget revenues. The function is implemented through tax control and tax sanctions, which ensure maximum collection of established taxes and create obstacles to tax evasion. Simply put, it is the collection of taxes in favor of the state. Thanks to this function, the main purpose of taxes is realized: the formation and mobilization of the state’s financial resources. All other taxation functions are derivatives of the fiscal function.

The distributive (social) function of taxation is the redistribution of public income (funds are transferred in favor of weaker and more vulnerable categories of citizens by imposing the tax burden on stronger categories of the population).

The stimulating subfunction of taxation is aimed at supporting the development of certain economic processes. It is implemented through a system of benefits and exemptions. The current tax system provides a wide range of tax benefits to small businesses, enterprises of the disabled, agricultural producers, organizations making capital investments in production and charitable activities, etc.

The disincentive subfunction of taxation is aimed at establishing, through the tax burden, obstacles to the development of any economic processes.

The reproductive subfunction is intended to accumulate funds for the restoration of used resources. This subfunction is performed by deductions for the reproduction of the mineral resource base, payment for water, etc.

The regulatory function of taxation is aimed at solving certain problems of the state’s economic policy through tax mechanisms. Within the framework of the regulatory function of taxation, three subfunctions are distinguished: stimulating, disincentivizing and reproductive.

The control function of taxation allows the state to monitor the timeliness and completeness of budget receipts of funds and compare their amount of financial resources.

The tax burden

A country's tax level is often measured as the total share of taxes in gross domestic product (GDP).

The actual tax burden on the economy is understood as the share of actually paid mandatory payments to the state in the country's GDP.

The difference between the nominal and actual burden characterizes the degree of tax evasion. The higher the rated load, the higher the deviation.

The tax burden on an enterprise should be understood as the ratio of the amount of taxes and deductions, the real payer of which is the enterprise, to the amount of profit of the enterprise.

The real payer of the tax is the entity that is:

the owner of the taxable object, when the obligation to pay tax arises from the very fact of the existence or emergence of the taxable object;

user of a taxable object, when the obligation to pay tax arises only when the object is in certain conditions of use.

The “tax burden” indicator in Russia is used to analyze the level of taxes paid by a business entity in order to control the level of payments and identify entities that potentially evade taxes.

The “tax burden” is calculated as the ratio of the amount of taxes paid according to the reporting of tax authorities and the turnover (revenue) of organizations according to the Federal State Statistics Service (Rosstat).

The maximum value of the indicator is established annually by sector of the national economy.

Still have questions about accounting and taxes? Ask them on the accounting forum.

Tax: details for an accountant

- Income tax in 2018: clarifications from the Russian Ministry of Finance

Establishing the specifics of payment by a self-regulatory organization of income tax on income in... /95452 The expression “may be taxed in a Contracting State” contained... generally determines the procedure for reducing the amount of corporate income tax subject to credit... /43473 Amount of foreign tax (an analogue of which is the Russian value added tax... non-operating income for the purposes of calculating corporate income tax. Since the taxpayer...

- The legality of using tax clauses using the example of personal income tax, VAT and income tax

The taxpayer and the transfer of taxes to the budget system of the Russian... are required to withhold the accrued amount of tax directly from the taxpayer's income... established by this paragraph. Payment of tax at the expense of tax funds... to comply with the deadlines for calculating and paying tax, tax paid with the specified violation... includes the amount of tax presented to the buyer by the seller, the amount of tax is allocated by the latter... of the contract, the buyer will be obliged to pay the tax, and to the supplier of the Russian organization ...

- Advance payments for income tax: procedure and terms of payment

An advance payment based on the tax rate and profit subject to taxation, ... in a manner that ensures uniform receipt of tax during the tax period (... an advance payment based on the tax rate and profit subject to taxation, ... in a manner that ensures uniform receipt of tax during the tax period (... the period is counted towards the payment of tax based on the results of the next reporting... taxpayers calculate based on the tax rate and the actual profit received,...

- On the consequences of reducing the amount of property taxes

The amount of insurance premiums, transport, land taxes, property tax, mineral extraction tax (any of... expenses of the initially calculated amount of land tax, corresponding to the provisions of the listed norms, ... expenses of insurance premiums, transport, land taxes, property tax, mineral extraction tax entails not... the obligation to submit an updated property tax return, but the occurrence... by identifying an overpaid amount of the said tax, the corresponding adjustment should be considered for...

- General and special income tax rates

Categories of taxpayers. Reduced rates on income tax subject to crediting... - SEZ residents rate of tax subject to crediting to the federal budget... on the implementation of activities the amount of tax is subject to restoration and payment... The Russian Federation may establish a reduced tax rate subject to crediting to the budgets ... has the right to apply reduced rates for corporate income tax subject to... Recipient of dividends Payer of income tax Income tax rate Subclause...

- And again about corporate property tax reporting

Provisions allowing to take into account when calculating tax a change in the cadastral value of an object of taxation... are supplemented by provisions that provide the possibility of calculating tax in the event of a change in the cadastral value... of the year movable property is excluded from the list of objects of taxation (Federal... the legislation of a constituent entity of the Russian Federation provides for the inclusion of tax on the property of organizations in the regional... submission of notification standards for tax deductions to local budgets; submission...

- New in the legislation on taxes and insurance premiums

... – in the proposed material. Administration of taxes and fees The Federal Law of... is excluded from the objects of taxation on the property of organizations (Letter... on the territory of the Russian Federation. Land tax Government institutions that are payers... which are used when calculating land tax in relation to land plots, . .. is used to calculate land tax in the event of a change in cadastral value... At the same time, the procedure for calculating tax if it is necessary to simultaneously apply...

- Tax on self-employed people from January 1, 2019 (part 2)

Income received by the taxpayer. Tax rate, procedure for transmitting information about... independently. The tax return is not submitted to the tax authorities... to the tax authorities through the “My Tax” mobile application, information about the calculations made. ... an indication of the application of the special regime “Tax on professional income”; names of the products being sold... the right of tax authorities to automatically write off tax from a bank account through... fulfillment of the obligation to pay tax, which apply in the event of...

- New environmental tax

Russia may have another tax that will replace various... necessary consumer properties. Payers of the new tax will be recognized as everyone who... environmental protection. The draft economic tax provides that during the tax period... the draft provides for the possibility of reducing the tax due to expenses incurred.... Thus, the differences between an economic tax and a fee are as follows... fee. The proceeds from the tax will be spent on various purposes...

- For 2018, you need to report on land tax in a new way

Changes are periodically made to the land tax legislation, as... the tax base and the amount of land tax. Cadastral number of the land plot" ... used when calculating land tax in relation to land plots, ... used to calculate land tax in the case of legal ownership of a land plot... used when calculating land tax in relation to land plots, ... full land tax rates and reduced land tax rates. Indicator for...

- Obtaining property tax benefits for individual entrepreneurs

Carrying out business activities subject to a single tax) (Clause 4 of Article 346.26 ... UTII in relation to objects subject to property tax for individuals included ... may receive tax exemption, but it is not explained how ... that the exemption from property tax in question is a benefit, but... the taxpayer discovered that he paid property tax to an individual entrepreneur in relation to... the tax inspectorate application for a tax recalculation But such a recalculation may be...

- Calculation of annual tax under the simplified tax system

The tax return and payment of tax for organizations is established not... the tax return and payment of tax for organizations is established not... the object of taxation “Income” is calculated as follows: For the object “... Income”, the amount of tax is reduced by the amount of insurance paid contributions...: the amount of the calculated minimum tax exceeds the amount of the single tax calculated in general... The difference between the minimum tax paid and the single tax calculated in general...

- Amendments to property tax reporting from 2019

Next - calculation), submission of a property tax declaration (hereinafter - the declaration), procedure... procedure for calculating and paying tax). The calculation of tax in section 2. Draws... the tax base and the calculation of the amount of tax in relation to the subject to taxation... will cease to relate to the objects of property taxation. Naturally, from... The procedure for filling out an advance calculation for property tax indicates numerous... about real estate subject to tax at the average annual value. Now...

- Property demolition and property taxes

Grounds for stopping the accrual of tax in relation to those located in... information: according to the company, additional tax assessment is unlawful, since the actual demolition (... the concept of “asset”) differs. Therefore, the property tax on the disputed object... gave the following arguments: payers of the property tax are recognized organizations... The Tax Code of the Russian Federation, which provides for the specifics of taxation of real estate objects, in relation to... will have an impact on the calculation of another tax - the property tax on individuals persons

- For a novice accountant about calculating a single “imputed” tax

Object of taxation. For the application of a single tax, the object of taxation is... taxation, a merchant who is a payer of the “imputed” tax has the right to use to confirm received... drugs. Accordingly, when calculating the tax, she needs to use the following indicators... months of the quarter, respectively. Reducing the tax amount. The amount of UTII calculated for... a taxpayer for which a single tax is paid. At the same time, taxpayers producing...

Or the operational management of funds for the purpose of financial support for the activities of the state or municipalities (Article 8 of the Tax Code of the Russian Federation).

According to the Tax Code of the Russian Federation, a tax is considered established only if the taxpayers and elements of taxation are determined, namely: the object of taxation, the tax base, the tax period, the tax rate, the procedure for calculating the tax, the procedure and deadlines for paying the tax. A concept close in meaning is a fee, the payment of which, according to Russian law, (unlike a tax) is not free of charge, but is one of the conditions for the performance of legally significant actions in relation to fee payers by government bodies and officials, including the granting of certain rights or the issuance of permits (licenses). ).

Tax legal relations are based on the powerful subordination of one party to the other. They presuppose the subordination of parties, one of which, the tax authority acting on behalf of the state, has the authority, and the other, the taxpayer, has the duty of obedience. The requirements of the tax authority and the tax obligation of the taxpayer follow not from the agreement, but from the law. The legal form of establishing a tax, the mandatory and compulsory nature of its withdrawal, and the unilateral nature of tax obligations are associated with the public legal nature of the tax and the state treasury and the fiscal sovereignty of the state. As a result, the dispute over failure to fulfill a tax obligation is within the framework of public (in this case tax) rather than civil law.

Doctrinal definitions of tax

Types of taxes

There are two types of taxes.

First type - income and property taxes: income tax and corporate profit tax; for social insurance and for the wage fund and labor (so-called social taxes, social contributions); property taxes, including taxes on property, including land and other real estate; tax on the transfer of profits and capital abroad and others. They are levied on a specific individual or legal entity and are called direct taxes.

Second type - taxes on goods and services: turnover tax - in most developed countries replaced by value added tax; excise taxes (taxes directly included in the price of a product or service); for inheritance; for transactions with real estate and securities and others. These are indirect taxes. They are partially or fully transferred to the price of the product or service.

There are also fixed, proportional, progressive and regressive tax rates. Fixed rates are set in absolute amounts per unit of taxation, regardless of the size of income.

Proportional - act in the same percentage of the tax object without taking into account the differentiation of its value.

Progressive rates suggest that the rate increases as income increases.

Progressive taxes are those whose burden falls more heavily on those with higher incomes.

Regressive rates suggest that the rate decreases as income increases.

A regressive tax may not lead to an increase in the absolute amount of budget revenues when taxpayer income increases. Depending on the use, taxes are divided into general and specific. General taxes are used to finance current and capital expenditures of state and local budgets without being assigned to any specific type of expenditure. Specific taxes have a specific purpose (for example, contributions to social insurance or contributions to road funds).

The most important tasks of tax policy in the current conditions

1. ensuring sufficient budget revenues to finance urgent social programs;

2. a sharp structural shift in economic proportions in favor of those industries that work directly to meet the needs of the population;

3. creation of the most favorable conditions for stimulating business activity.

The actual tax burden on the economy is understood as the share of actually paid mandatory payments to the state in the country's GDP. The tax burden varies significantly across countries. Underdeveloped countries (which do not have a strong social security system) are characterized by a low tax burden, while developed countries are characterized by a relatively high tax burden (reaching up to 60% of GDP in Sweden in some years). The exception is some developed countries in Southeast Asia, where the tax burden is relatively low. In Russia, the tax burden is about 42%, which is slightly below the average level of developed countries (higher than in the USA, but lower than in Germany, see).

There are actual and nominal tax burdens. Nominal tax burden is the share of mandatory payments in GDP that taxpayers must pay if they fully comply with tax legislation. The difference between the nominal and actual burden characterizes the degree of tax evasion. The higher the rated load, the higher the deviation. When the rated load exceeds a certain level, the deviation becomes massive and the actual load decreases. The point at which the actual load is maximum is called the Laffer point. It is believed that the nominal tax burden should be slightly below the Laffer point, because higher values force taxpayers to violate tax laws.

In developed countries, the nominal and actual load are close to each other. In many underdeveloped countries, the nominal burden is very high, as a result of which entrepreneurs can always be caught violating tax laws. This leads to the dependence of entrepreneurs on officials and the development of corruption. According to official data from the Ministry of Finance of the Russian Federation, the nominal tax burden in Russia is 41%. However, most economists provide different data. Thus, according to research by the analytical center of the same Ministry of Finance - the Economic Expert Group, the nominal tax burden in Russia is 55-60% of GDP.

Ways to evade taxation in Russia

- It should be noted that high taxes provoke entrepreneurs to hide funds from taxation, which leads to the development of the shadow economy. Thus, in Russia from 1998 to 2008, a scheme for receiving money under a fictitious agreement, called “cash out”, was widespread.

- Many specialists [ Who?] drew attention to the fact that from 1991 to 2009 in Russia there was no need to use schemes called “money laundering”, because the origin of capital, for the most part, did not arouse the interest of either the state or citizens.

- A relatively rare tax reduction scheme for Russia is working with offshore companies, primarily due to the large supply of “cash out” schemes and the relative ease of carrying them out in Russia; also, the use of offshore zones requires large working capital.

see also

Links

- Official publisher of the Federal Tax Service

Wikimedia Foundation.

2010.

See what “Taxes” are in other dictionaries: In this world, the only inevitable things are death and taxes. Benjamin Franklin If you break the rules, you get fined; if you follow the rules, you are taxed. Lawrence Peter Taxpayer employer government. Taxpayers are victims of war... ...

Consolidated encyclopedia of aphorisms Mandatory payments levied by central and local government authorities from individuals and legal entities. Taxes serve as one of the means of regulating economic processes and economic life. According to the level of collection of taxes, they are divided... ...

Financial Dictionary Mandatory payments levied by central and local government authorities from individuals and legal entities that go to the state and local budgets. Taxes are the main source of funds entering the state treasury.... ...

Economic dictionary taxes - pay a decision, compensation taxes are collected action, liability to pay taxes decision, compensation reduce taxes change, little reduce taxes change, little reduce taxes change, little...

Verbal compatibility of non-objective names TAXES, mandatory payments levied by the state (central and local authorities) from individuals and legal entities to state and local budgets. They are divided into direct ones, which are taxed on income and property (income tax, tax... ...

Modern encyclopedia

Big Encyclopedic Dictionary Mandatory payments levied by the state (central and local authorities) from individuals and legal entities to state and local budgets. They are one of the forms of financial relations that ensure distribution and... ...

Political science. Dictionary.

Over the long history of the formation and development of the state, a great many different taxes have been invented. In the old days, when rulers did not really care about their political image, there was no limit to their imagination in coming up with something for which they could rip off extra money from their subjects. For example, taxes were introduced on racehorses and carriages, velvet and lace, furs and jewelry, on unusual types of buildings, balconies, windows, and chimneys.

However, we will have to wander for a long time in the intricacy of many taxes if we do not choose the main grounds for their division. For these reasons, current taxes are divided into:

· direct and indirect;

· federal, regional and local;

· taxes from individuals and legal entities.

So, first of all, all taxes differ in the methods of collection: direct and indirect. Direct taxes include income and property taxes (income and property taxes), and indirect taxes include taxes on circulation and consumption. The payer of direct tax is the owner of the property and the recipient of the income; The payer of the indirect tax is the consumer of the product, to whom the tax is transferred through an increase in price.

The effectiveness of direct taxes depends on the ability of citizens and enterprises to make certain designated payments in accordance with the amount of income, available property, etc. This method of taxation has always been associated with violent measures (coercion, fines, litigation, etc.). Citizens pay direct taxes very reluctantly, because they represent direct deductions from what they could, without taxes, consider their property. Hence the multiple violations of tax legislation - even criminal offenses.

Indirect taxes are a different matter. In this case, money is taken into the treasury from the population in a subtle way: producers of goods and traders are taxed, this tax is included in the price of manufactured and sold products, and thus the tax burden is borne by those who buy these goods. With indirect taxation, the amount of payment to the state is hidden from the eyes of the taxpayer, so the state sometimes shamelessly increases these taxes, simultaneously demonstratively reducing direct taxes by several percent. And the population easily “buys” into such tricks of clever financiers who tend to plug budget gaps by reaching deep into the pockets of ordinary citizens.

Direct taxes depend on the personal performance of citizens and are guided by it. Indirect taxes focus on things, not persons. They are levied on producers, traders, and transport owners, but in the end, these taxes are paid by citizens who buy goods and use services. These taxes are less fair than direct taxes because the poor and the rich pay the same amount of such tax: of course, if the poor have the opportunity to buy the goods subject to the indirect tax at all. The invisibility and “softness” of indirect taxes lead to the fact that in many modern states they are in a privileged position.

Compared to direct taxes, indirect taxes are primitive and crude, but they are easier to obtain. In ancient times, collectors of indirect taxes from traders and merchants often did not even know how to read and write. However, they knew the score perfectly well. And this was enough to collect tax on goods: he counted the number of bags or jugs, took a certain amount of money from the owner for each - that’s all the work.

It has long been noted that one or another type of tax prevails in countries depending on the level of their economic development. In developing countries, the majority of tax revenue comes from indirect taxes. It’s clear why: the population is poor, not burdened with property, people’s incomes are small. Direct taxes will not provide large revenues to the budget. And even the poor can pay a premium to the price of goods to compensate for indirect taxes. After all, they also need to eat, buy modest clothes, etc. Direct taxes are of greater importance in economically developed countries with a wealthy population with a relatively high educational qualification.

The Tax Code of the Russian Federation divides taxes into federal, regional and local.

Taxes and fees established by this Code and obligatory for payment throughout the territory of the Russian Federation are recognized as federal. Currently, federal taxes include the following:

1) value added tax;

2) excise taxes on certain types of goods (services) and certain types of mineral raw materials;

3) tax on profit (income) of organizations;

4) tax on capital income;

5) income tax from individuals;

6) contributions to social extra-budgetary funds;

7) state duty;

8) customs duties and customs fees;

9) tax on subsoil use;

10) tax on the reproduction of the mineral resource base;

11) tax on additional income from hydrocarbon production;

12) fee for the right to use fauna and aquatic biological resources;

13) forest tax;

14) water tax;

15) environmental tax;

16) federal licensing fees.

Regional taxes are taxes and fees established by the Tax Code of the Russian Federation and the laws of the constituent entities of the Russian Federation and mandatory for payment in the territories of the corresponding constituent entities of the Russian Federation. These taxes include:

1) tax on property of organizations;

2) real estate tax;

3) road tax;

4) transport tax;

5) sales tax;

6) gambling tax;

7) regional license fees.

Local taxes and fees are those established by the Tax Code of the Russian Federation and obligatory for payment in the territories of the relevant municipalities. These include the following taxes:

1) land tax;

2) tax on property of individuals;

4) inheritance or gift tax;

5) local license fees.

2.3 Main taxes collected in Russia

Despite the fairly large number of taxes and other obligatory payments, the most significant part in the income of budgets of all levels is made up of income tax, VAT, excise taxes, payments for the use of natural resources and personal income tax. They account for over 4/5 of all tax revenues of the consolidated budget.

Let's take a closer look at what each of these taxes is.

Value added tax

Added value includes mainly wages and profits and is practically calculated as the difference between the cost of finished products, goods and the cost of raw materials, materials, semi-finished products used for their production. In addition, the added value includes depreciation and some other elements. Thus, the tax is on added value created at all stages of production and defined as the difference between the cost of goods sold, works, production and distribution services and the cost of material costs charged to costs.

The following are recognized as VAT taxpayers:

Organizations;

Individual entrepreneurs;

Persons recognized as tax payers in connection with the movement of goods across the customs border of the Russian Federation, determined in accordance with the customs code of the Russian Federation.

The tax base for this tax is the gross value at each stage of the movement of goods from production to the final consumer, i.e. only part of the value of goods, new, increasing at the next stage of the passage of the goods. Hence, the objects of taxation are turnover from the sale of goods on the territory of the Russian Federation, including those for production and technical purposes, both self-produced and purchased externally, as well as work performed and services provided.

Objects of taxation are also goods imported into the territory of Russia in accordance with established customs regimes, excluding humanitarian aid.

The law defines a list of goods (work, services) exempt from tax. This list is uniform throughout the Russian Federation.

The following are exempt from value added tax:

Services in the field of public education related to the educational and production process,

Tuition fees for children and teenagers in various clubs and sections,

Services for maintaining children in kindergartens, nurseries,

Care services for the sick and elderly,

Funeral services of funeral homes, cemeteries and crematoriums, as well as related enterprises;

Services of cultural and art institutions, religious associations, theatrical and entertainment, sports and other entertainment events.

Research and development work carried out at the expense of the state budget, and contractual work carried out by public education institutions are exempt from paying value added tax.

Excise taxes are an indirect tax included in the price of the product and is paid by the buyer. Excise taxes, as a value added tax, came into force on January 1, 1992, with the simultaneous abolition of turnover tax and sales tax.

Excise tax payers are all enterprises and organizations located on the territory of the Russian Federation, including enterprises with foreign investment, collective farms, state farms, as well as various branches, separate divisions that produce and sell the above-mentioned goods, regardless of their form of ownership and departmental affiliation.

The object of taxation is the turnover (cost) of excisable goods of own production, sold at selling prices, including excise tax. Such goods subject to excise taxes include: wine and vodka products, ethyl alcohol from food raw materials, beer, tobacco products, cars, trucks with a capacity of up to 25 tons, jewelry, diamonds, crystal products, carpets and rugs products, fur products, as well as clothing made from genuine leather. The excise tax amount is taken into account in the value added tax base. Certain goods are not subject to excise taxes. Excise tax rates are approved by the Government of the Russian Federation and are uniform throughout Russia.

Personal income tax is one of the main types of direct taxes and is levied on the income of workers.

Effective January 1, 2001 In the second part of the Tax Code of the Russian Federation, the system of taxation of personal income has changed significantly. The new tax concept is aimed at reducing the tax burden through a significant expansion of tax benefits for individuals, the introduction of a minimum tax rate of 13% on income received from the performance of labor and equivalent duties, and the abandonment of total income using progressive tax rates. However, not all income is planned to be taxed at this rate. Thus, cash prizes, lottery and betting winnings, unusually high deposit payments and insurance claims will have to be taxed at a rate of 35%. Those. income, the receipt of which is not related to the performance by an individual of any labor duties, work, or provision of services.

A rate of 30% is established for income received in the form of dividends and for income received by individuals who are not tax residents of Russia.

Taxpayers of personal income tax:

1. Individuals who are tax residents of the Russian Federation. They pay tax on income received both within the Russian Federation and abroad.

2. Individuals who are not tax residents of the Russian Federation. They pay tax on income they receive from sources located in the Russian Federation.

The object of taxation is income received by taxpayers from sources in the Russian Federation and/or from sources outside the Russian Federation - for individuals who are tax residents of the Russian Federation, or from sources in the Russian Federation - for individuals who are not tax residents of the Russian Federation.

It is planned to significantly increase the amount of deductions from taxable income. In addition, the innovation is that it will be allowed to reduce taxable income for expenses on paid education and medical care. In this case, not only the costs of paying for education by the taxpayer himself, but also his children will be taken into account. Medical expenses include, among other things, the purchase of medications. At the same time, the legislator established a limit on reducing the tax base. It cannot be more than 25,000 rubles. per person per year for each type of expense.

Unified social tax (contribution)(UST) is credited to state extra-budgetary funds - the Pension Fund of the Russian Federation, the Social Insurance Fund, the compulsory medical insurance funds of the Russian Federation - in order to mobilize funds to realize the right of citizens to state pension and social security and medical care.

At the same time, control over the correctness of calculation, completeness and timeliness of contributions to the funds paid as part of the unified social tax is carried out by the tax authorities of the Russian Federation.

The procedure for spending funds paid to the funds, as well as other conditions associated with the use of these funds, are established by the legislation of the Russian Federation on compulsory social insurance.

It should be especially noted that one hundred contributions for compulsory social insurance against accidents at work and occupational diseases are not included in the Unified Social Tax and are paid in accordance with federal laws on this type of social insurance.

Tax payers according to Art. 235 parts of the second Tax Code of the Russian Federation have been recognized since 2001:

Making payments to employees, including organizations; individual entrepreneurs; tribal, family communities of small peoples of the North, engaged in traditional economic sectors; peasant (farm) farms; individuals;

Those who do not make payments to employees, including individual entrepreneurs; tribal, family communities of small peoples of the North, engaged in traditional economic sectors, peasant (farm) households, lawyers.

If the subject of tax relations simultaneously belongs to several categories of taxpayers, he is recognized as a tax payer on each individual basis.

In 1998, the country's budget system received 526 billion rubles, including 194 billion rubles into the federal budget, tax payments, and 332 billion rubles into territorial budgets.

The task set by the State Tax Service of Russia to collect taxes into the federal budget for 1998 in the amount of 154.1 billion rubles was fulfilled by 116.7% (for 1997 - by 91%). The level of receipt of taxes and fees in the country's budget system in relation to GDP in 1998 was 19.6% and in the federal budget - 7.2%.